The year-end audit

Open books, personal integrity, and relationship with the truth

Everyone hates audits. I mean, who wants to be audited? It’s almost a dirty word. But in modern society, audits are critically important. Any massive financial misbehavior you know about, you know because they were audited. Enron. Bernie Madoff. Trump taxes. Sam Bankman-Fried. People are able to get away with fraud for as long as no one checks on them. In fact, fraud exists because people think they can hide things. They think no one is checking. The audit is the necessary check in the system that keeps us honest.

I’ve been thinking about this because of this Washington Post advice column, where a reader wrote in about her fiance (apparently a lovely guy) having secret credit cards and lying about the amount of debt he has. One comment made me laugh because it’s so true:

“He’s not bad with money; he’s bad with truth and honesty. It just manifests itself monetarily.”

That might be said of all of us. I sometime ask my students that if they died and there was a financial autopsy done, what would it reveal? If someone looked at your finances and didn’t know you, what would they say your values were? What did you prioritize and care about? Reviewing your spending every year keeps you honest. If you have a partner, it’s a really good exercise in vulnerability and transparency.

Being an open book

When I ran Portland Underground Grad School, I had open book accounting, which meant the public look at the books. Anyone, teachers, students, employees, could see what money was coming in and what was going out. Showing our books that gave us greater accountability (ha! get it?) and full transparency to the general public. Everyone knew what cost what and who was being paid what. I felt like it was the most honest way to run a company that served the community.

In my personal life, I do a personal audit at the end of every year. How did I spend my money? Am I being honest with myself on where I spent my money and who gets it? It’s about having a relationship with the truth. It’s also simply interesting to see what you spent money on.

Doing is is relatively easy if you have a credit card. In full transparency, here’s my EOY spending for 2022:

$17,259 of credit card expenses this year.1 Very similar to previous years. One level deeper dive:

Services are mostly household stuff: electricity, water, internet, cell phone bill. Also business subscriptions for School of Financial Freedom like Discourse, Squarespace etc.

Restaurants: my major “fun” expense. I spent $2,000 on my 50th birthday weekend!

Merchandise: Mostly groceries and Amazon purchases. Some of it for the house, some of it pure consumerism. Also, I made the Great Transition and bought a Macbook and iPhone, so that was around $1,000.

$1,000 per year on on another credit card which has my car insurance and trash autopayments on it.

I spent $21k on home repairs: a new roof and repainting the exterior of the house, and having some plumbing issues with the basement. As FF alumni know, I don’t have a mortgage, thanks to my younger self saving and buying a home in cash. But if you have a house, you need to reserve money for maintenance, even if you don’t have a mortgage. This year was a big year for maintenance. I’ve had $25k on maintenance in nine years I’ve owned the house (previous expenses: new refrigerator, washer, and dryer, also plumbing issues). The universal recommendation is budgeting 1-4% of the value of the house for maintenance, which does not include renovations, which is really consumption.2 Note: this means if your house has 5% “home appreciation” every year, but you have to spend 3% in maintenance, after 2% (or more) of inflation, you probably are not gaining any “value” in the house. That's why you need to be careful about "appreciation" as you account for real estate in your nest egg. Digression aside, I amortize my annual home maintenance as $3,000 per year.

I also paid $4,500 in property taxes this year. This keeps going up and up.

I donated $2,000 to the Center for Action and Contemplation and to Homeboy Industries.

Because I have so little income, I had free health care this year on Oregon Health Plan. Really grateful for that because I broke my heel and tore my Achilles. Surgery and physical therapy would have been $20,000+ but I got it covered. Again, grateful.

All in all, I spent about $27,000 in 2022, almost exactly what I spent in 2021. This is a breakdown of what the average American household spends, $68k a year, and because I’m single, a breakdown of what the average single person spends, $61k.

More thoughts

Doing an annual audit is about having a relationship with the truth. Otherwise known as reality. With your values. Interestingly, 65%-73% of Americans report that they don't have a budget. In other words, two-thirds of Americans are unconscious about how much they are spending. This unconsciousness is higher in younger generations.

A big chunk of any budget is spent on housing. Until I bought my house, I almost always lived with roommates, spending $300-$600 per month (I know inflation etc). Housing density, i.e. living with others, is the biggest win in any budget.

Inflation! I’m sometimes asked, “How do you keep to your budget when inflation went up 8% this year?” Well, if the cost of my Needs went up, I simply spend less on my Wants and decide to be more grateful for when I spend money on my Wants. As Aldous Huxley said, “Most human beings have an almost infinite capacity for taking things for granted.” Sticking to your Wants budget is resisting your ingrained and expanding entitlement.3

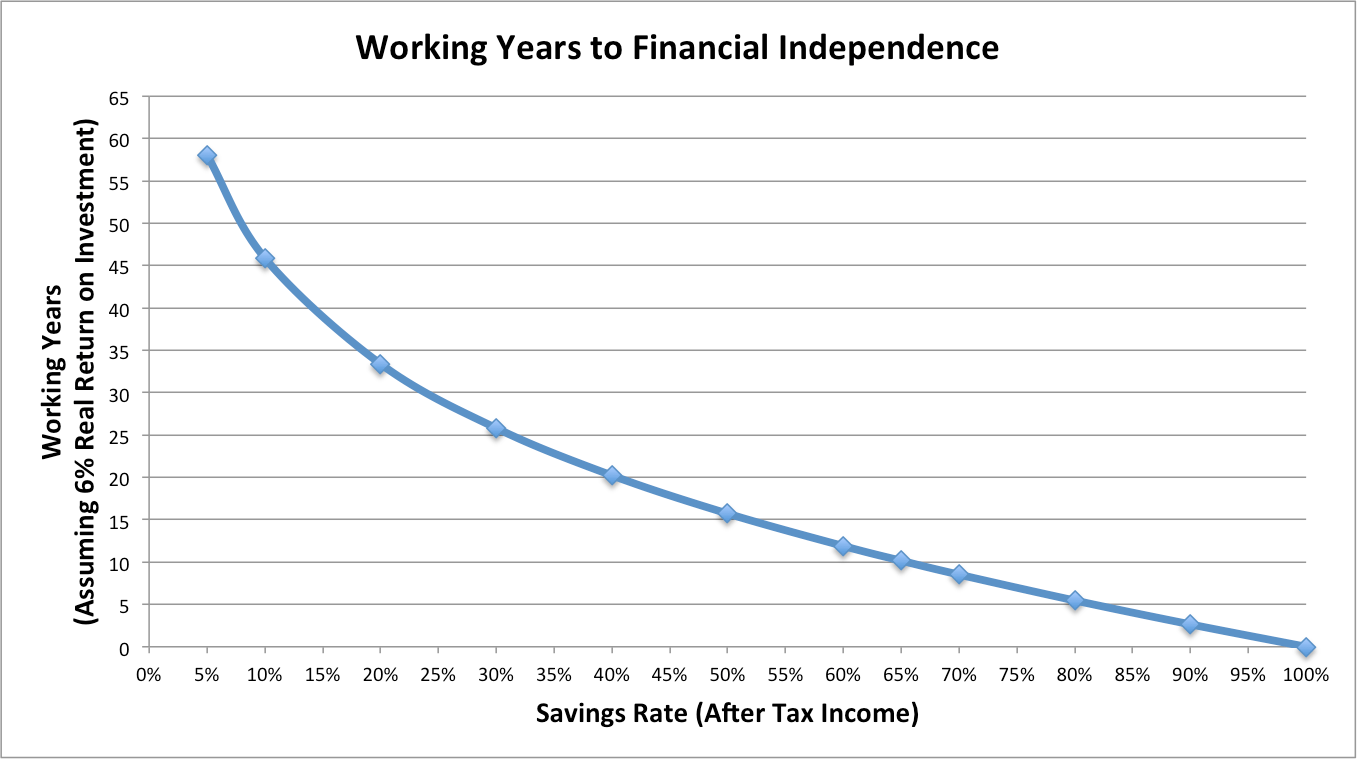

Left unspoken in my own budget is that idea of a savings rate. That’s because I’m not saving for retirement anymore. But it shouldn’t be left out of yours! It may be the most important thing. Your savings rate drives your future financial security. If you look at the chart below, you’ll see that if you save 20% per year, you’ll reach financially independence in 35 years. And just as importantly if you save 5% per year, you’ll have to work 60 years. Most people won’t be able to work 60 years, even if they want to. Ageism is real.

I’ve been thinking recently that I should spend more money. I’ve trying to let go of my money vigilance. I’m a child of Chinese immigrants who fled the Communists, leaving almost everything behind. Spending money doesn’t feel gaining fun, it feels like losing security. Old childhood money scripts affect all of us, me in this particular way. The book Die with Zero has gotten me thinking about not spending is a lost opportunity of living fully. I should maximize life enjoyment instead of preserving wealth. But it’s really complex because…

Environmental factors. I believe we have an ethical obligation to live lightly on earth. My carbon footprint is about 20 tons a year. Biggest chunks of my footprint is air travel and eating meat, both of which I feel conflicted about. But because I spend less money overall, my footprint is 29% smaller than the average Portlander. You can check your carbon footprint with the Berkeley Cool Climate Calculator. For all of you who say you care about climate change, this is also about having a relationship with the truth.

Also, I feel conflicted about the assumed relationship between spending money and “maximizing your life enjoyment.” Even the word “maximizing” has a masculinist, mechanic feel to it. I’m not trying to “maximize” life, that’s part of the ideology that’s screwing us. So yes, I’m struggling with Die with Zero.

“Rest comes when we become more by doing less, when we don’t allow the urgent to crowd out the important”― Frank Ostaseski, The Five Invitations

We tell ourselves lies, big and small. And that maladjusts us to life. The end of year audit is not only having a relationship with the truth, it’s about having a relationship with reality. Krista Tippett once said, “My working definition of spirituality is befriending reality.” Choosing to audit your own spending is befriending reality.

Knowing what you spend your money on helps you know what you value and what you value less. My friend Annie says the whole point of spirituality is gaining an increased intimacy with the world. Personal finance is gaining intimacy with what you really love and choose to offer your time and attention to.

If a year-end audit is a relationship to the truth, the issue then becomes are you living it out. This is your moment of self-reflection and self-awareness. Does your spending, and your carbon footprint, match what you say your values are? Where are you living a life of integrity, and where can you improve?

A how-to guide to a 10 minute personal audit

If you have a life partner, grab them. Pour a couple glasses of wine, hold holds for a moment, make it romantic. If you’re single, put on your PJs, and get under a blanket on the couch.

Pull your laptop out and go to your credit card website to check your spending. There should be place where it categories your spending over the year.

Figure out where else you spend money. Do you have automatic withdrawals for things like your mortgage or rent? What checks do you write? Paypal or Venmo? Cash withdrawals? All these things are tracked, somewhere.

Total all of that and you should have your total spending. Now you have the truth. Does it match your values? Are you living in integrity?

One level deeper

Look at your bank balances. How do they look compared to a year ago?

Look at your investment accounts. Forget for a second whether the net worth has gone up or down (your investments probably went down this year, unlike the previous three years). Instead check how much you put into your account for investments. That’s your savings rate!

Think about what your goals are for next year. Hint: hold the line on your spending while increasing your income. You need cost-of-living adjustments from your employer. Can you look for a promotion, increase your skills, get another credential, or ask for a raise? Most of that should go to increasing your savings rate.

Happy new year everyone! As the Chinese would say, have a prosperous and healthy 2023!

If you read this newsletter, you probably know I hate credit cards (I even have a project that fights against credit card companies). Even if you pay them on time on your end, they take 3% from every transaction, from the vendor. So I just gave $520 to a credit card company, just be living. But it’s near functionally impossible to pay bills or buy internet thingies without it.

See my previous post Home Renovations: Cost or Investment?

Of course if you work, you could get cost-of-living adjustments from your employer and adjust your budget to inflation. Also, raises and promotions, but I advocate you not spend that (spending creep) and use most of that for improving your savings rate.